Building a Greater Britain 🇬🇧

Building a Greater Britain 🇬🇧

To make the UK the birthplace of more scalable innovation, we must start with our culture and mindset

Silicon Valley is the leading light of “the West”. But it is not the first tiny area of the world to deliver outsized innovation, and it will not be the last.

For much of its history, Athens was either preparing for war, at war, or recovering from war. But in the window between the Persian and Peloponnesian Wars, from 454 to 430 B.C., the city was at peace, and it flourished. The Athenians were “not very numerous, not very powerful, not very organized,” as the classicist Humphrey Kito noted, but they nevertheless “had a totally new conception of what human life was for, and showed for the first time what the human mind was for.”

Like Silicon Valley today, ancient Athens during this brief period became a talent magnet, attracting smart, ambitious people. A city with a population equivalent to that of Wichita, Kansas, it was an unlikely candidate for greatness: Other Greek city-states were larger (Syracuse) or wealthier (Corinth) or mightier (Sparta). Yet Athens produced more brilliant minds—from Socrates to Aristotle—than any other place the world has seen before or since.

Source

The Athenians brought us the western basis of democracy, science, philosophy, writing, taxes, schools and contracts. Not bad.

After Athens, Rome brought us civil engineering, books, the postal service, town planning, the roots of modern medicine and, of course, military innovation.

The 15th century Renaissance in Florence and Venice brought with it step-changes in art, literature, science and business (modern accounting and banking in particular), as well as the roots of modern humanism.

More recently, the industrial revolution, whose epicentre was London (supported by Liverpool, Sheffield, Leeds, Manchester, Birmingham et al.), brought us innovations in textiles, metalwork, steam power, machinery, chemicals, glassmaking, mining, transportation, literacy, economics and finance.

L.S. Lowry’s The Canal Bridge, a vivid, energetic depiction of Britain during the industrial revolution.

Some would argue that these centrums come into being by chance. This makes them hard to replicate, and fleeting. Indeed, Athens’ seat at the head of the table only lasted a quarter century. However, in recent years, both Israel and Singapore have succeeded in “intentionally” creating environments that foster innovation. Before them both, though, came the Shenzen Special Economic Zone in China, perhaps the leading example of this very deliberate approach.

So it is possible. How do we do it?

If we look across history, we can see a pattern. It is clear that a thriving ecosystem of innovation requires a high density of 4 crucial ingredients:

🤓 Talent: well-educated, technical individuals willing to take financial and personal risk by challenging convention

🏛️ Institutions: good legislative infrastructure and world-class academic research, supported by state funding

💸 Capital: a well-developed investment environment, and sufficient capital available for alternative investments

🤝 Culture: closely connected community with shared values of open-mindedness, trust, graft, risk-appetite, frontier mentality and collaboration

When mixed, these four tasty ingredients produce an elixir that only gets more delicious with time. Thanks to network effects, the components of the ecosystem beget more of the same thing that made them great - the talent attracts more talent, which attracts more capital, and so on.

The UK has solved most of this problem:

Talent

We have world-class technical and business talent from across the globe densely located in London and the surrounding area. The desire is there too: according to a recent survey by Ebuyer (a company owned by one of Britain’s great entrepreneurs), 80% of Britons want to start a business.

Institutions

We have the Golden Triangle, which boasts four global top 10 universities. 15 universities in the United Kingdom (which is only 57% of the land area of California), are in the global top 100.

Capital

We are the global centre of financial services, and a top 5 city for billionaires-in-residence. SEIS and EIS provide fantastic tax breaks for early-stage investors, incentivising risk-taking.

So what gives? Because something is clearly missing…

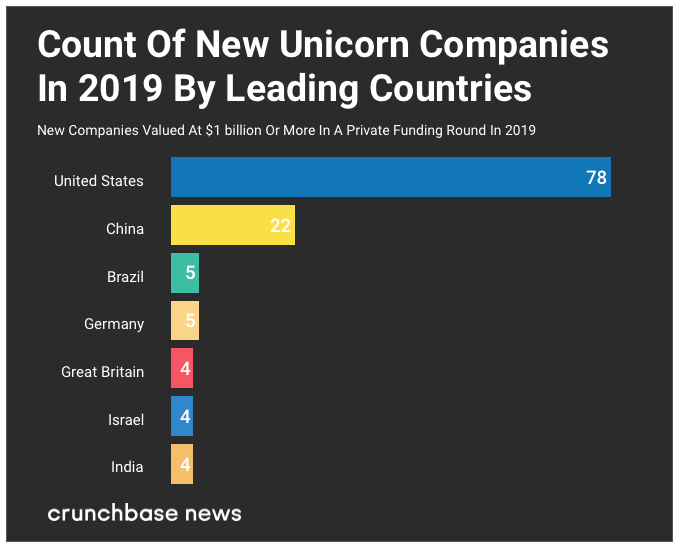

There were as many new unicorns (private companies valued at over $1bn) in Israel -pop. 8.9 million - as there were in Britain - pop 66.7 million - last year.

We need a cultural shift

What we are missing in the UK currently is the culture and mindset that creates large companies doing game-changing things. This is evident in the way that investors, founders and the state (the three key participants of an innovation ecosystem) think, act and interact.

Investors

In a recent podcast, Charlie Songhurst (the British ex-head of corporate venture at Microsoft, an investor in over 450 startups) spoke about the difference in mindset between East Coast and West Coast investors in the USA, and how this had affected the rise of Silicon Valley. He spoke first about the fact that California was in essence a “new nation” born after WWII, and that this pioneer spirit oriented the people towards new technology, the growth industry. But Songhurst also believes the Valley’s success is down to something much simpler - trust:

I think the second part is differences in the nature of trust and zero sum-ness. Partly because financial markets are in the traditional sense zero-sum. One person’s stock alpha is another person's negative alpha. East Coast investing has this sort of sense of, I need to beat the other person, I need to get a deal. And that has led to sort of lower trust between participants. And the West Coast - maybe it's sort of part of California, hippie culture tradition coming in - has this very high sense of trust. And if you look at these – the convertible note, if you look at the sort of letting the founder make decisions without supervision – these things can only emerge in a very high trust culture. I'm not sure you can build trillion dollar market cap companies without that high trust culture

I think if you don't have it, you end up building something with a billion dollars and then arguing over how to sell it or how to optimise it. And you don't get that sort of, “je ne sais quoi” aspiration that you see in all the trillion market cap companies, all of which are on the West Coast.

Songhurst also believes East Coast investors assess opportunities differently, and that this limits their ability to pick big winners:

And then I think there's some interesting little sort of cultural foibles … maybe [due to] what people do as analysts between the age of 21 and 23. So if you spend your time between 21 and 23 building Excel models, you tend to think more about numbers. And so you tend to have a much better intuition for margin economics. And so where the East coast is often right … it's that they correctly identify businesses with shaky unit economics, but fast revenue growth and “good” product market fit. And they're like: “Look, you have product-market fit, but only because you're giving away $100 to $90. So of course you've got good product market fit.”

I'll give the sort of counterpoint where West Coast investors do very well, is where you have a product lead that doesn't get evinced in the numbers immediately, but it's such a sort of tactile and visceral experience when you use it, you have to make an imaginative leap to turn that into numbers. And there are two examples. One is the iPhone, and I was doing some investigations for Microsoft at the time. And it was always easier to talk back competitors than talk about yourself because you're less likely to say something you shouldn't. So you always try and steer the conversation to talking about Apple, Google or something. And one of the things you realized is there was a bunch of investors that sort of thought Apple was overvalued when it was sort of a hundred, $200 billion market cap, because they took the TAM of Nokia and said, “even if they take all Nokia's market share, this business can't be big because phones only sell whatever it was back then”.

And they couldn't intuit the increase in pricing power that you are going to get from turning the phone into a computer. And the West Coast, VC community immediately intuited that…

And so one thing that's taught me, is trying to be smarter than other people is very hard and it doesn't work very often. Trying to have an insight that you get because you sit in a different information flow just seems exponentially easier.

British investors are, inherently, “East Coast” thinkers. Just 8% of UK venture capital investors have experience working in a startup, vs. 60% in the USA. So what experience do they have? For the main, it is consulting or investment banking - industries where Excel is king, and zero-sum is the name of the game.

This is not to say that these skills are not highly valuable. But we need more investors in the UK with technical and product experience. We must foster better flow of information between the different knowledge bases. Many people working in tech do not to have masses of money to invest, but they can spot the qualitative things that Songurst describes. On the other hand, the people doing the investing often view investments in startups through a very quantitative and overly risk-averse lens. I am still baffled by the number of investors that want to see a discounted cashflow for a pre-revenue business.

There are also a lot of issues around diversity. I’m not going to belabour this point - it has been covered extensively - but there is good evidence that improving diversity in the investment world can improve returns.

Founders

Founders are the second piece of the puzzle. Good founders are difficult to define, but there seem to be some consistent traits. Sam Altman, former president of Y-Combinator and now CEO of OpenAI, paints the following picture:

So how do you identify future greatness?

It’s easiest if you get to meet people in person, several times. If you meet someone three times in three months, and notice detectable improvement each time, pay attention to that. The rate of improvement is often more important than the current absolute ability (in particular, younger founders can sometimes improve extremely quickly).

The main question I ask myself when I meet a founder is if I’d work for that person. The second question I ask myself is if I can imagine them taking over their industry.

I look for founders who are scrappy and formidable at the same time (a rarer combination than it sounds); mission-oriented, obsessed with their companies, relentless, and determined; extremely smart (necessary but certainly not sufficient); decisive, fast-moving, and wilful; courageous, high-conviction, and willing to be misunderstood; strong communicators and infectious evangelists; and capable of becoming tough and ambitious.

Some of these characteristics seem to be easier to change than others; for example, I have noticed that people can become much tougher and more ambitious rapidly, but people tend to be either slow movers or fast movers and that seems harder to change. Being a fast mover is a big thing; a somewhat trivial example is that I have almost never made money investing in founders who do not respond quickly to important emails.

What’s often missing in the UK, in my experience, is the grit and the hunger. It is nowadays popular to decry the American culture of “workism”, and the Brits love to laugh at how cocky and outspoken Americans can be, but there is an uncomfortable truth - you don’t build big, successful, highly innovative companies from nothing without being stubborn, slightly pushy and willing to suffer hardship.

These are not character traits that come naturally to British people. We are raised to be polite to the point of boring. And perhaps, thanks to generous social support, the hunger to go out and succeed is not quite so consuming as it is in the States. It is interesting to note that in the USA, 25% of new companies are started by immigrants, who make up 13% of the population. These are people with dreams, drive and little to lose.

But Altman believes that these character traits are learnable.

In my time at Crowdcube, I spoke with hundreds of entrepreneurs, and the thing that impressed me about the most successful ones was that they never moaned. They could have complained that investors didn’t “get it”, or that raising money was harder here than elsewhere. But they just got on with things. Unfortunately, many more thought it was reasonable to value their pre-revenue DTC football boot startup at £4 million, and that investors were fools if they couldn’t see that this was the next Nike. In a nation where investors are naturally more risk-averse and unfamiliar with the territory, this mindset is harmful.

The State

The final cultural shift needed is in government response. To date, the response to the way technology is fundamentally reshaping society has been…underwhelming. David Cameron’s foray into tech with Silicon Roundabout, whilst well intentioned, did not really cut the mustard. We need the same change in thinking from government as we are asking of investors. What is really needed is money. Risky money to fund cutting-edge research in the fields of science, technology, engineering and mathematics (STEM).

Dominic Cummings has long been a proponent of significant state investment in a semi-autonomous DARPA-like organisation (the American defence agency that thought up the internet). The objective of this agency should be to invest in high-risk projects with potential for power-law ROI (just like VC), and significant positive social impact. Essentially, the state needs to step in where VC is still too risk-averse.

This is not really about big bucks in government terms, although spending will need to be significant. It is more about assembling small groups of incredibly exceptional people and trusting them to get on with things.

SEIS and EIS, the investment schemes which offer significant tax benefits to investors, should be maintained. They are a godsend. It may be worth extending SEIS (50% cash back in tax relief to investors on the first £150k a startup raises) to a higher value for extremely knowledge-intensive technology. If done right, this would help us to really push investors in the direction of more radical innovation.

We should also be more savvy and focused on attracting technical founders from the rest of the world to our shores with open arms. In my short time at Enterprise Ireland in Russia, we had some success in attracting talented STEM founders to Ireland simply by making a bit of noise in the Moscow tech scene and being friendly. A legacy of the Soviet Union’s excellent education system, Eastern Europe is a veritable goldmine of technology talent - just look at the success of development agencies like EPAM (Belarus - 37,000 employees, market cap $17.8 bn) and George Soros-backed Ciklum (Ukraine - 3,500 employees, valuation unknown) . See also Seedcamp’s golden child UiPath, now valued at $10.2 billion (Romania). The government should be bringing this talent to Britain, not scaring it off.

Lastly, addressing regional inequality is an area the state, the technology sector and the financial sector can cooperate on. I grew up in Scunthorpe and went to school in Hull. As a son of doctors, I was shielded from the sharper edges of these places. But it was plain to see that people had suffered dramatically as a result of Britain’s deindustrialization. It has created deep wounds that will take time to heal. How to bring wealth and togetherness back to these local economies?

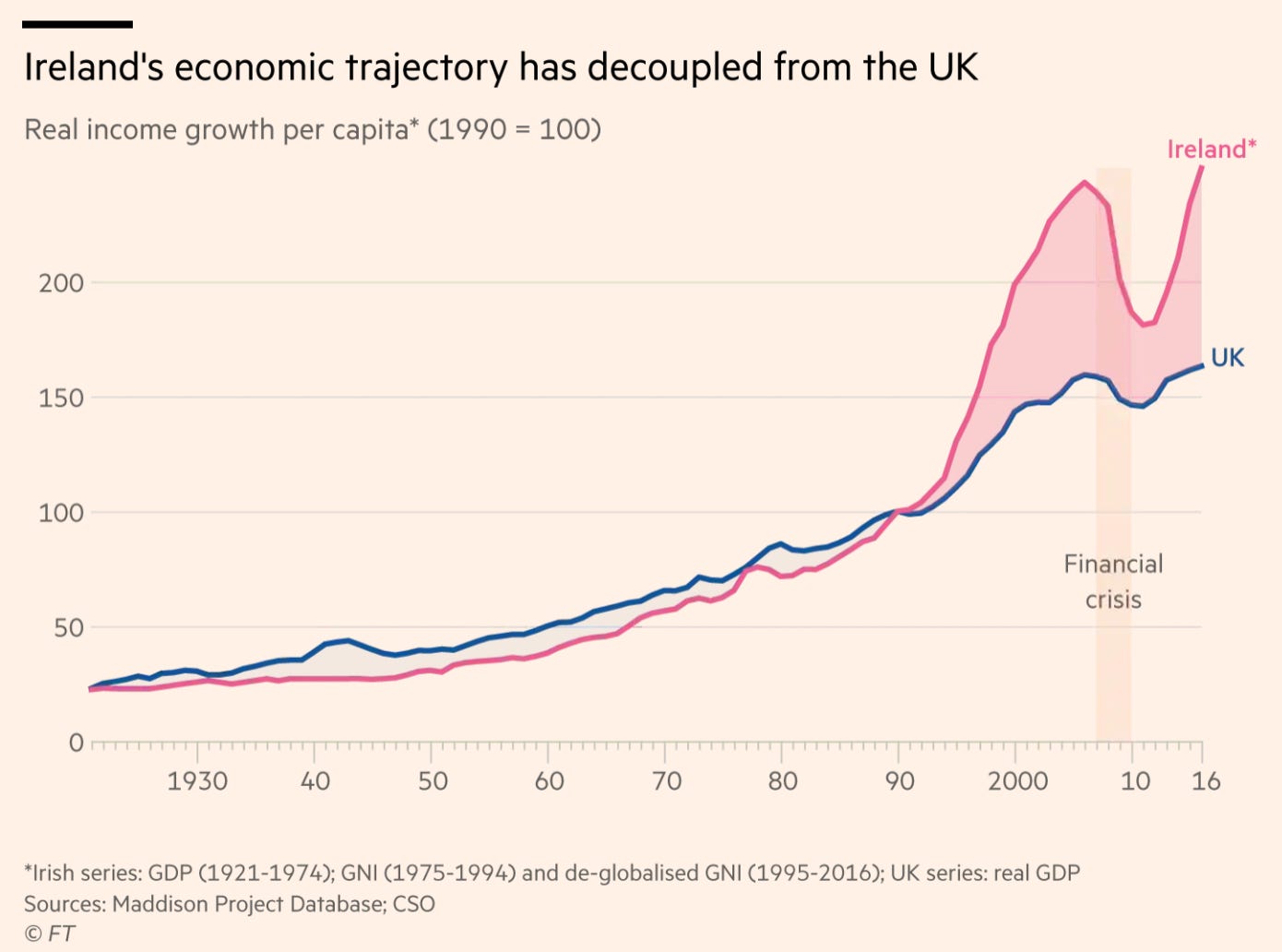

COVID and the dawn of remote work might help (you can buy a two bedroom apartment in Hull for £45k), the Northern Powerhouse initiative may be useful (somehow - what is it exactly?), but perhaps we can learn from the Chinese and the Irish examples. If we significantly drop corporation tax regionally for innovative enterprises, the impoverished North will attract technology firms and the highly skilled, big-spending workers that come with them. We can do the same in Wales, Northern Ireland or wherever else. Outside of the cooperative constraints of the EU, this is possible. People’s views on this are mixed, but if we look at the example of Ireland (once Europe’s orphan in rags, now richer than the UK), we can see that it works.

Source

Corporation tax in Ireland is 12.5%, and 6.25% if you are an R&D heavy business. Adopting a similar policy for every business not headquartered in the south (and HQ means office, staff, etc.) might help spread the UK’s centre of gravity more evenly.

What is to be done?

I cannot speak with conviction on policymaking - my proposals on the subject of tax are ideas for discussion.

However I can, hopefully, speak for founders and investors.

I’ve struggled at times to clearly articulate what we are building at Odin. We’ve toyed with the idea of raising a VC fund. But the UK does not need more capital allocators - it needs better capital allocation. It needs to support more brilliant people with great ideas. This is true whoever they are, and wherever they are from. For this to succeed, we need to reset our thinking:

The Athenians also hastened their demise by succumbing to what one historian calls “a creeping vanity.” Eventually, they reversed their open-door policy and shunned foreigners. Houses grew larger and more ostentatious. Streets grew wider, the city less intimate. People developed gourmet taste. The gap between rich and poor, citizen and noncitizen, grew wider, while the sophists, hawking their verbal acrobatics, grew more influential. Academics became less about pursuing truth and more about parsing it. The once vibrant urban life degenerated.

Sound familiar?

At Odin, we are building a curated community of smart, open-minded, high-performing people from the worlds of science, technology and finance. This community is a true reflection of modern Britain, with all its wonderful variety - there are working class lads from Liverpool in there, and daughters of Nigerian immigrants. There are rich bankers and scrappy founders. There are physicists, historians, linguists, mathematicians, economists and psychologists. There are Oxbridge graduates and people without degrees. There are friends from across the European continent, and further afield.

We are working on scalable, technology-driven ways to create meaningful connections between these people and we are laser-focused on building an environment of high trust.

By facilitating the free flow of information, ideas and capital between members of this community, we can - like the Athenians - strive to be “adventurous beyond our power, and daring beyond our judgement”.

This is what is needed to create a Greater Britain.

A special thank you to Nicolas Colin of The Family, whose writings and thinking on this problem I have drawn on not just in this short essay, but in how we have approached setting up Odin. ✌️🇫🇷

Great post Paddy... but all that’s needed for a cultural shift is a few big exits (which contribute to talent, capital and institutions...). This was also the case in Silicon Valley 20 years ago. Spotify is the first big example of this in Europe. Other will follow. UK is on the right track, we’re just a couple decades behind Bay Area. We’re still a decade ahead of the rest of the world though and it’s never been cheaper or easier for talent to move, so we should catch up quickly with the right policies.